With the new administration hard at work, egg prices causing people to panic like rustled hens, and tariffs of uncertainty in the air, many are worried about a potential recession. The market is feeling some turbulence. While no one can predict the future with 100% certainty, it’s always wise to be prepared. The key to feeling financially independent in uncertain times isn’t panic; it’s having a solid plan in place.

So, how do you prepare for a recession? How can you position yourself to weather a recession if one happens? How can you come out stronger on the other side?

A lesson I rehash again and again is that a strong financial foundation is built on consistency, not knee-jerk reactions. If you already have a solid financial plan, stick to it. A well-structured plan accounts for economic downturns and helps you navigate them without making drastic, emotional decisions based on the feelings of the moment.

Where Not to Keep Your Money During a Recession

Now, there are some straightforward strategies to take if a recession occurs, as not all financial moves are created equal. One common mistake is keeping too much money tied up in speculative investments that may take years to recover. If the market is shaky, these types of investments can be particularly risky. Similarly, taking on high-interest debt, like credit card balances, is not advisable. During a recession, these types of debts can put an unnecessary strain on your finances.

First and foremost, you must be aware of where your money is housed. You could expose yourself to unnecessary risk if you’re keeping large amounts of cash in uninsured or unstable financial institutions. Finally, putting too much money into assets that are difficult to liquidate, such as real estate or collectibles, can leave you in a bind if you suddenly need access to funds. During uncertain times, liquidity and stability should be your top priorities.

What Not to Do During a Recession

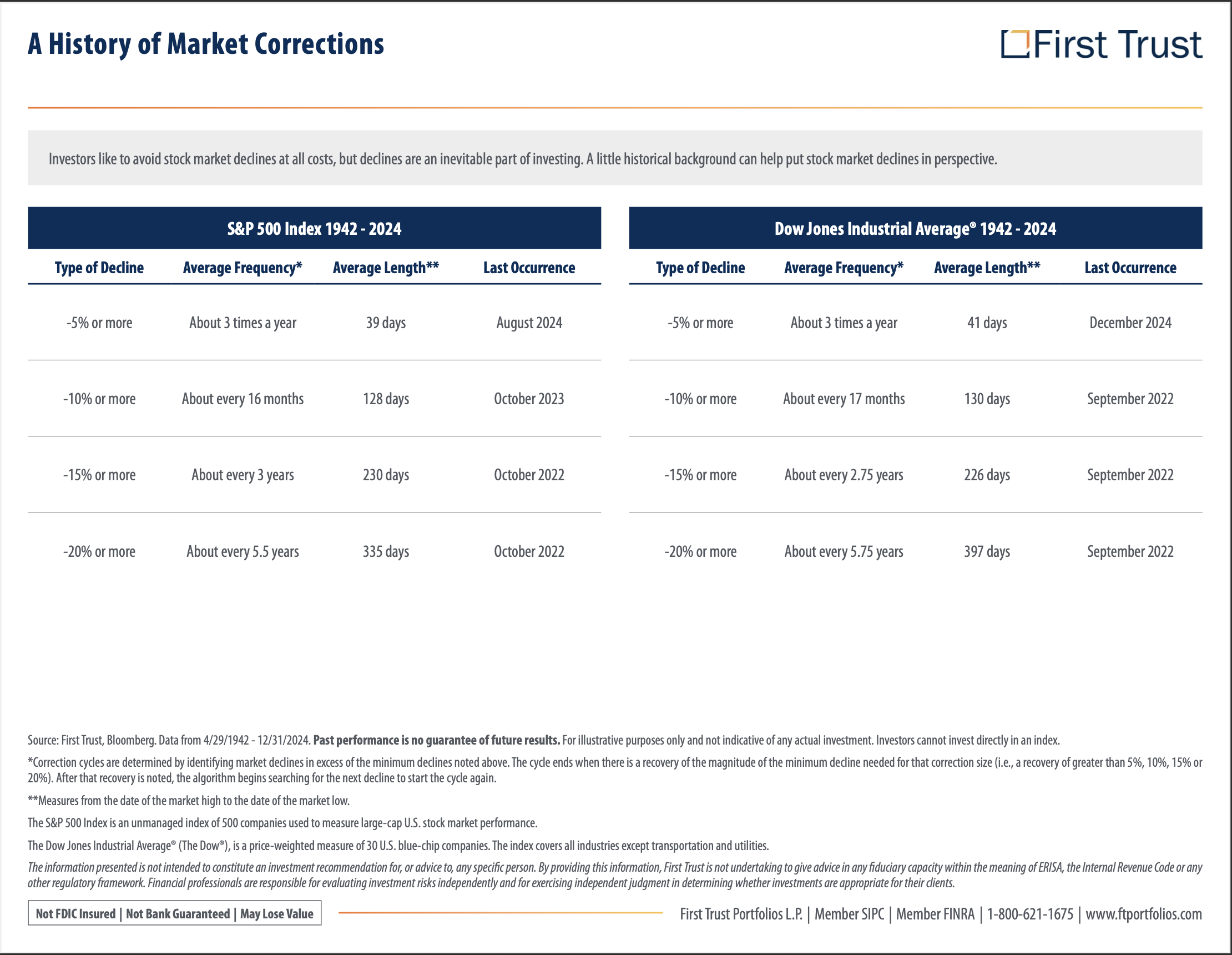

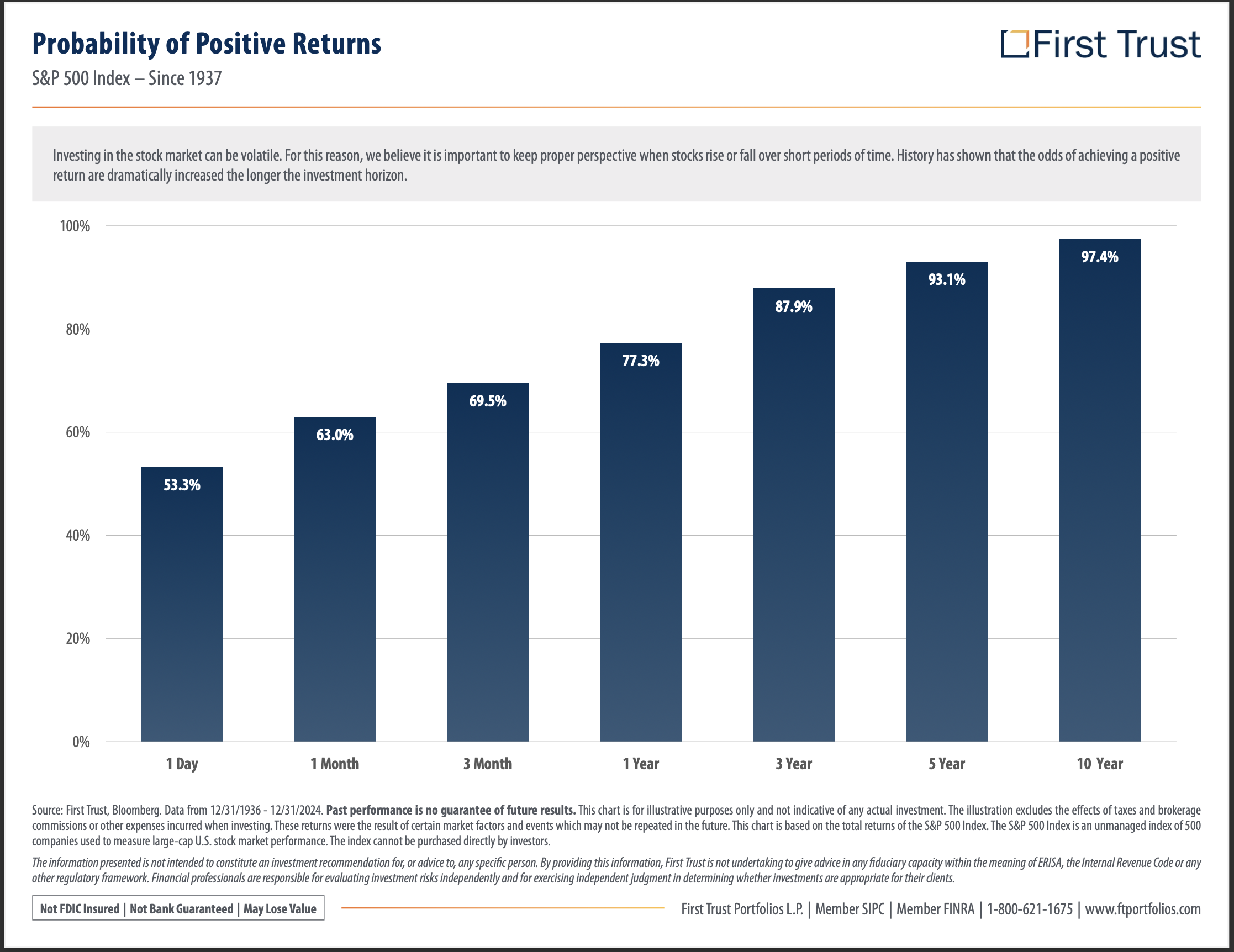

Making financial decisions based on fear is never a sound idea and often leads to costly mistakes. One of the worst things you can do is panic-sell your investments. The stock market has always rebounded over time, and those who stay invested through downturns typically recover. Selling at a loss locks in those losses permanently, making it much harder to regain stability when the market recovers.

Another common mistake is trying to time the market. Many people attempt to predict when stocks will hit rock bottom or peak, but even seasoned professionals struggle with this; everyone would be rich if it were easy! Instead of making impulsive moves, focus on maintaining a long-term investment strategy.

I can’t stress this enough: pay attention to your personal economy rather than being consumed by national headlines and the talking heads’ takes and predictions. While broader economic conditions matter, your own job security and financial well-being should be your focus. You can’t control how global events play out, but you can fully grasp your own microcosm.

Right now, economic fluctuations may be causing concern, but history tells us one thing: the market has always rebounded over time. A long-term investment strategy accounts for market cycles.

The Three-Bucket Investment Approach

If you’re unfamiliar with it, this would be a good time to introduce you to my three-bucket investment/retirement strategy. A well-diversified financial strategy can help you weather economic storms. My three-bucket approach is structured to provide stability, income, and long-term growth—even during shaky moments. The benefit of this approach is that it allows your plan to determine your portfolio allocations rather than picking an arbitrary 60/40 split.

- Cash Bucket

This bucket is your safety net, filled with liquid assets like cash, short-term bonds, or money market funds. It should cover two to three years of living expenses, helping you avoid selling investments when markets are down. If the economy takes a hit, this bucket ensures access to your finances without tapping into long-term investments.

- Income Bucket

Designed to generate steady returns, this bucket helps replenish your Cash Bucket over time. It holds conservative investments like bonds, dividend stocks, fixed annuities, and CDs. This bucket can provide stability because it covers your essential expenses without forcing you to make drastic financial moves.

Check out my Cash Alternatives Guide to learn more about different ways to optimize your cash and income buckets.

- Long-Term Growth Bucket

This bucket is your engine for future savings, focused on higher-risk investments like stocks that can outpace inflation over time. Since this bucket isn’t meant to be touched for at least ten years, you can ride out market volatility without panic. When the economy recovers, these investments should fuel the other two buckets.

By structuring your investments this way, you avoid being forced to sell assets at a loss when markets are down.

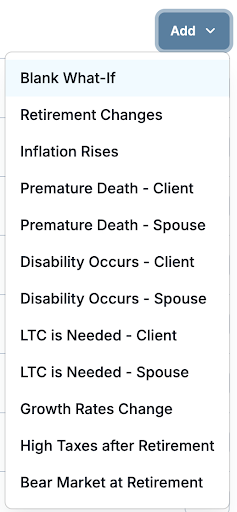

The “What If” Scenarios

Your financial plan should include “what if” scenarios. If a recession hits, will you still be on track? With a solid financial plan, “what if” scenarios are factored in case unforeseen circumstances arise. For example, recessions often bring job instability, making it essential to assess your job security. If your industry is volatile (like sales or commission-based roles), increasing your cash reserves can provide extra security. Aim for 6-12 months’ worth of expenses in liquid savings if you are accumulating assets and 2-3 years’ worth of your income gap if you live off your investments.

Whenever I work with my clients to develop a plan, it is tested against 9+ “what-ifs; we can add whatever custom what-if a client is concerned about. The what-ifs stress test the base plan and identifies gaps that can be proactively addressed.

How Do You Prepare for a Recession? – Stay Calm and Carry On

The most important thing you can do is avoid panic. Economic cycles are a normal part of financial history and have in the past have always led to recovery. By sticking with a solid foundational financial plan, you can stay on your course to your goals and keep the turbulence tolerable.

If you would like to discuss your financial plan, let’s talk! Click the link below to book a call. As a family financial planner, my door is always open.

The S&P 500 is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States. Indexes are unmanaged and cannot be invested in directly. (102-LPL)

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors. Indexes are unmanaged and cannot be invested in directly.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. (26-LPL)

Investing involves risk, including the possible loss of principal.